Agriculture in 2016 is a story of intuition and data. For centuries, farmers have been successful in part by relying on their good intuition passed from generation to generation. Many farmers know when to plant, which crops will yield the most bushels per acre and the highest profits, and they trust their gut to know when the timing is just right to harvest.

But, intuition can be elusive. That’s where data enters the picture. Guided by satellite imagery, the farmer today is able to accurately spray just the right amount of fertilizer in just the right portions of the field. Paired with drone technology, farmers can accurately monitor field nutrient information, view data on pesticide use and forecast weather.

Commodity Prices

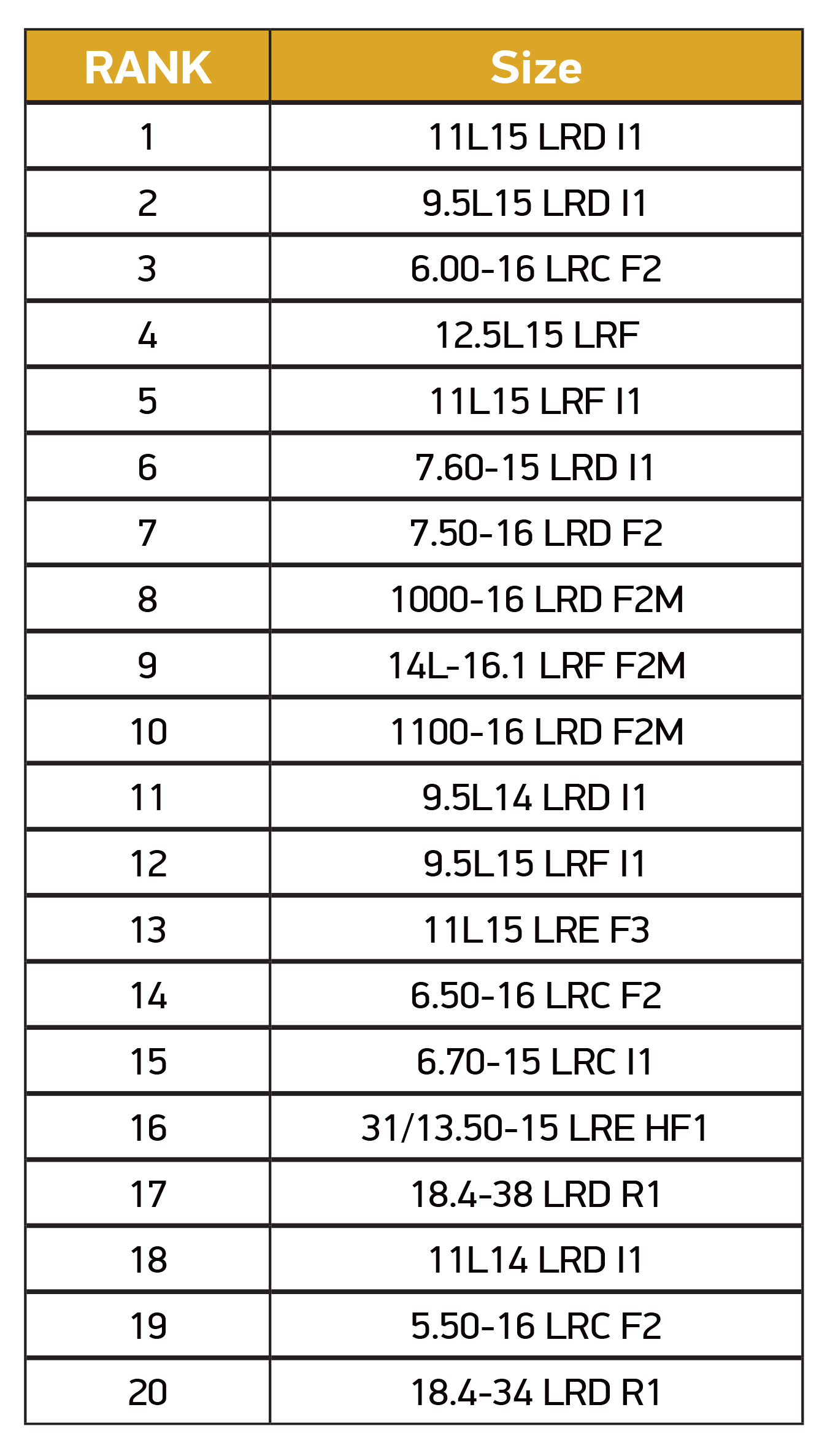

For the ag tire dealers selling to those farmers, the story is similar. Decade after decade, many of the best tire dealers and cooperatives in the country passed along knowledge to the next generation of leading ag tire dealers. Knowing which brands and sizes to stock (see figure 1), how to hire and train the best field service technicians, and knowing how to negotiate the optimal spring tire order were all paramount to the success of the best ag tire dealers. However today, the leading dealers pair what their gut tells them with the story their data tells them. Let’s put this to the test.

Crop prices are awful, right? The experts tell us it’s basic supply and demand. An overabundance of crop inventory has driven prices per bushel to historic lows. Allow me for a moment to defer to one of my literary heroes, Mark Twain, who famously said, “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

Here’s what we know that is so. According to the National Agricultural Statistical Service, the average price of corn from 1999 through April 2016 was $3.48 per bushel. From September 2015 through April 2016, the average price for a bushel of corn was $3.62. That’s a $0.14 per bushel premium over the 17-year average. Of course ethanol production during the past several years as played a part in inflating corn prices, but that’s a story for another day.

Because corn could be just an outlier in the data, let’s take a look at soybeans. The beans will tell the real story. From 1999 through April 2016, the average price for a bushel of soybeans was $8.56. Starting January 2016 through the end of April 2016, the average price for a bushel of soybeans was $8.71. That’s a premium of $0.15 per bushel. As the man said, it’s what we know for sure that just ain’t so that ends up getting us into trouble.

Input Costs and Income

There’s a lot of volatility in the markets right now. If you follow the news, you already know that Britain voted to pull a “Brexit” from the European Union and France is already talking about making its own “Frexit.” The financial markets don’t like uncertainty so they’ve been very volatile. That volatility includes commodities.

The oil cartels of OPEC, led by Saudi Arabia, made the decision to keep their feet on the oil-production pedal. That led to a historic glut of oil, driving down oil prices 21.8% in the past 12 months. Bad time to be a Chevron shareholder, but great time to be an American farmer or farm tire dealer. According to the USDA, corn planted for all purposes in the U.S. is estimated at 93.6 million acres in 2016. That’s up more than 6% from 2015. Interestingly, soybean and wheat acreage is expected to be down about 1% and 9%, respectively, while cotton acreage should be up about 11%.

In terms of input costs, total production expenses are projected to be down about 1% in 2016, including feed (-5%), fertilizer (-5%), and fuel (-15%). Elsewhere, government payments under the price loss coverage (PLC) and agricultural risk coverage (ARC) programs are projected to be up by 31%, the highest payment levels since 2006. The PLC and ARC programs were authorized by the 2014 farm bill.

But farm income is down, right? The plight of the average farmer in America will surely show up in the data. According to the U.S. Census Bureau, the average household income in America is somewhere around $53,000 this year. Average farm income in 2016 is projected at $128,000, which is actually up 3.8% from 2015. It’s what we know for sure that just ain’t so.

However, farm asset values for 2016 are projected to be down about 2% from 2015, reflecting increases in farm debt and weaker land values, according to the 2016 U.S. Farm Income Outlook.

Industry leader John Deere has taken a beating on Wall Street, but its fundamentals actually look pretty good given the circumstances. Total revenue at Big Green is down about 21% from 2013, but cash flow is actually up quite a bit to $4.16 billion. Even revenue is starting to tick north with second quarter 2016 revenue at $2.34 billion.

Manufacturers of big iron seem to be benefiting at least to some degree from Section 179 of the farm bill, which now permanently allows farm operations to depreciate up to $500,000 in a single year on the purchase of qualifying new equipment up to a total max equipment purchase of $2 million per year. I guess American economist and Nobel laureate Milton Friedman was right when he said, “Nothing is so permanent as a temporary government program.”

Expansions, Tariffs, Mergers and Acquisitions

Elsewhere in the world of agriculture, low interest rates created an environment of inexpensive capital while market performance created a perfect storm for mergers and acquisitions. Late 2015, Trelleborg announced its $1.25 billion all-cash acquisition of CGS Holding, which includes the Mitas and Cultor farm tire brands. Earlier this year, Trelleborg also made its first foray into manufacturing tires in the U.S. with its brand new 430,000-square-foot facility in Spartanburg, S.C. Meanwhile, Yokohama recently closed its $1.1 billion acquisition of Alliance Tire Group.

2016 has thus far proven to be a tough year for Indian-based manufacturers. In June, the United States Department of Commerce announced its preliminary subsidy on Indian OTR (and agricultural) manufacturers. BKT will absorb a 4.7% countervailing duty, Alliance Tire was hit with a 7.64% tariff, while all other Indian manufacturers will cough up an extra 6.17% at U.S. customs and border patrol. The final determination is slated for October, but could be pushed back and is retroactive for 90 days. As of the time of writing, no decision had been made on anti-dumping cases. Thus far, it seems that the manufacturers have largely been able to absorb the additional costs in some cases by becoming the official importer of record themselves, rather than the wholesalers.

Led by Titan Tire and the United Steelworkers, the DOC’s ruling should be a boon for Titan’s business as well as domestic manufacturing in general. That is, until you consider that Titan hasn’t actually been profitable since 2013 and has lost $155 million in the past two fiscal years. Titan International President and CEO Morry Taylor should be all right, unless activist investor and Carl Icahn protégé Mark Rachesky starts to get anxious. Head of MHR Capital, Rachesky took a 10.9% stake in Titan in early 2014. According to Yahoo Finance, MHR Capital now holds just over 8 million shares, or almost 15%, of the company. Will the bell toll on “The Grizz” before he can steer Titan back to profitability or will Taylor pull off the turnaround of the decade in 2016? Time will tell.

Replacement Farm Tire Sales

Paired with favorable oil costs and uncertainty in commodity markets, farmers seem to be outfitting existing iron with new rubber. Published industry metrics and market share statistics are usually highly skewed and tend to be based on poor information, but the replacement farm tire segment seems to be pointing in the right direction with unit volume increasing in low double-digit percentages. Of course, unit volume and top-selling sizes are highly regional by nature, which should also be taken into consideration.

Leading farm tire dealers must follow their intuition, while allowing the data to tell the story. Certainly there are some headwinds facing the agricultural industry, but the future looks brighter than ever for both farmers and farm tire dealers despite the volatility, emotions, and Brexits of the world, confirming what John Pierpont Morgan, founder J.P. Morgan & Co., once said: “Any man who is a bear on the future of this country will go broke.”