Recent trends in vehicle miles traveled are encouraging but perhaps offset by other statistics that loom as indicators of another rough patch for the U.S. economy and the aftermarket. In this article, we share results of a survey of the impact of COVID-19 at companies across the aftermarket, then touch on “best practices” that shop owners have implemented while navigating the pandemic.

Good News – Mileage is Back to Pre-Pandemic Levels

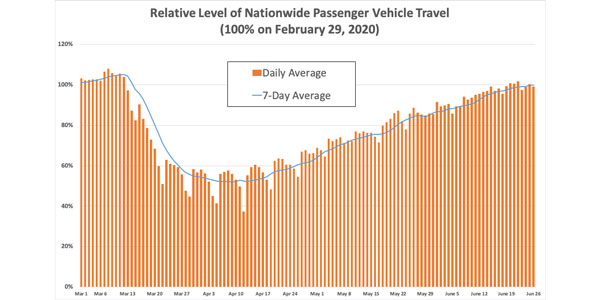

As of late June, vehicle travel has steadily ascended to pre-pandemic levels—since mid-April, passenger vehicle travel has gradually climbed back up to “normal” levels as states and municipalities have re-opened.

Not-So-Good News – COVID-19 Incidence Rising

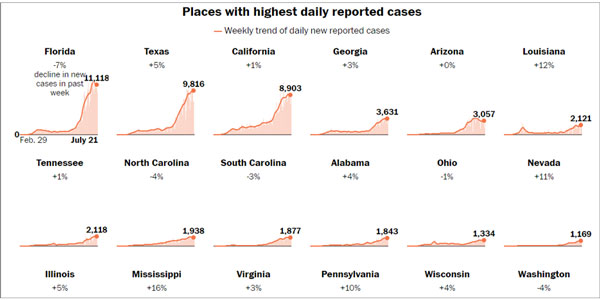

After flattening from April to early June, COVID-19 incidence rose sharply at the end of June and into July. At the beginning of August, there were nearly 4.8 million cases across the U.S, according to the Washington Post.

As documented in the media, cases grew rapidly in the West and South in late June/July, particularly in California, Texas, Florida, Georgia and Arizona.

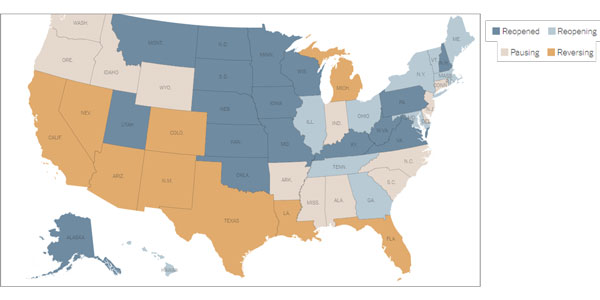

State Reopenings

Based on the changing dynamics of disease spread in each state, several have recently paused their efforts to re-open, or even reversed course to limit activity. For example, Arizona, California, Texas and Florida have scaled back operations for bars, beaches, cafes, nightclubs and gyms in an effort to mitigate disease spread and overburdening healthcare facilities. As of July 22, California, Nevada, Arizona, Colorado, New Mexico, Texas, Louisiana, Florida, and Michigan have reversed their reopening plans, according to The New York Times, while a dozen other states are pausing their reopening plans.

Age Group Considerations

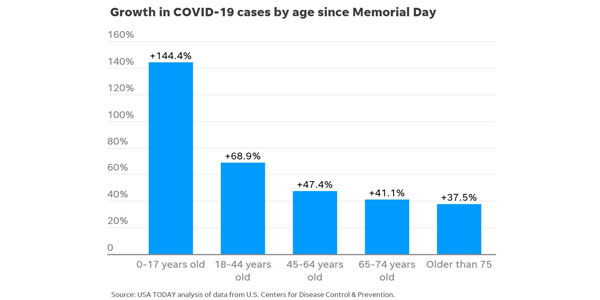

Of concern is the rise in COVID-19 cases in younger generations – incidence has increased more rapidly since Memorial Day among those under 45 years old. Since Memorial Day, growth in COVID-19 cases has grown by 144% for ages 0-17 years and 69% for ages 18-44 years, compared to only 38% for age 75+ years

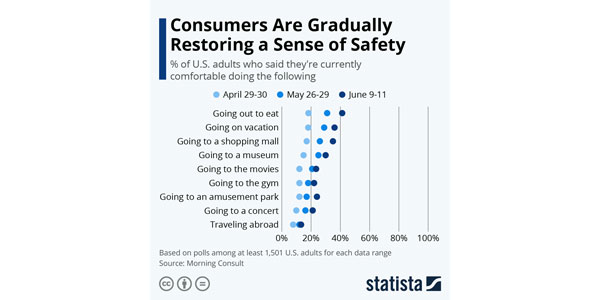

This is of concern as businesses have gradually reopened throughout the summer and as individuals have engaged in more activities outside their home. As the pandemic has progressed, individuals have become gradually more comfortable with engaging in “typical” activities like dining out, traveling for leisure, and going to a shopping mall, but still hesitant to attend movies, work out at a gym, or travel abroad.

Alongside the public’s willingness to engage in individual activities is the acceptance of risk at an organizational/societal level. Market research firm Ipsos finds that Americans are eager to get back to work despite the continued risks associated with the virus: 53% of U.S. adults agree with businesses reopening even if COVID-19 isn’t fully contained, versus 43% who disagree.

Industry Considerations

While individuals are gradually venturing out more, the increase in cases, particularly in Southern and Western states, is leading to mandates to restrict business activity. This is likely going to reduce vehicle activity and negatively impact the national economy.

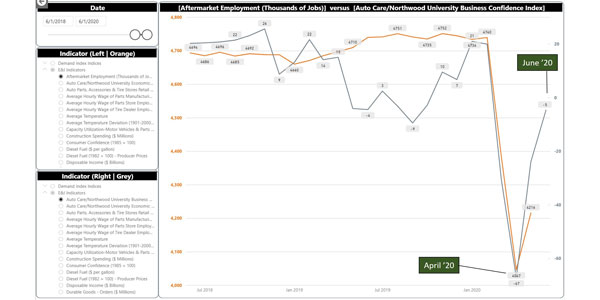

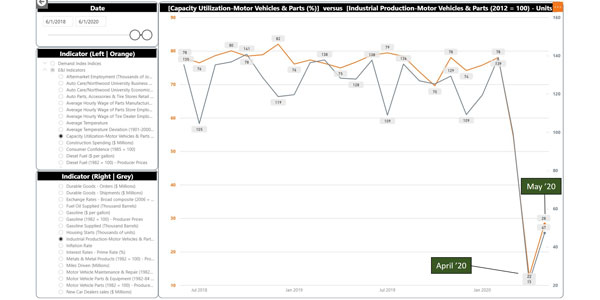

Looking at a few of the industry indicators available in the Auto Care Association’s TrendLens platform, employment and business confidence dropped significantly in April, then began rising in May/June.

Similarly, capacity utilization and industrial production for motor vehicles and parts fell significantly in April, then began climbing back in May.

Pandemic Impact on Industry

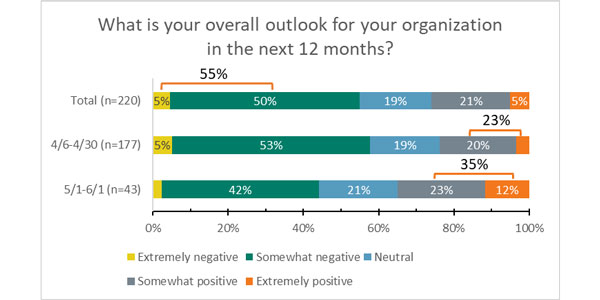

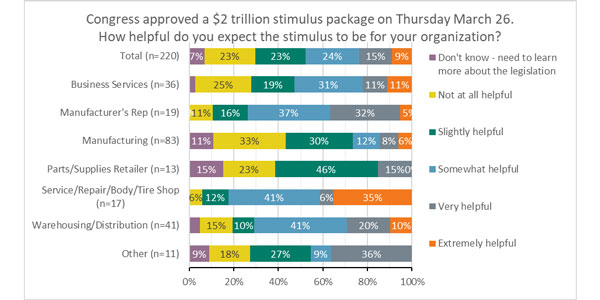

Auto Care has been surveying association members since early April to gauge the pandemic’s impact on the industry. Based on 220 responses, while outlook for the next 12 months leans somewhat negative (55% are “somewhat” or “extremely negative”), sentiment has brightened more recently. One-third of auto care organizations participating in May have a “somewhat” or “extremely positive” outlook (35%), versus one-quarter of organizations participating in April (23%), as seen in Fig. 1.

Larger companies are slightly more pessimistic (59% are “somewhat” or “extremely negative” versus 53% for companies with 1-500 employees), and manufacturing companies even more so: 67% are “extremely negative” (6%) or “somewhat negative” (61%).

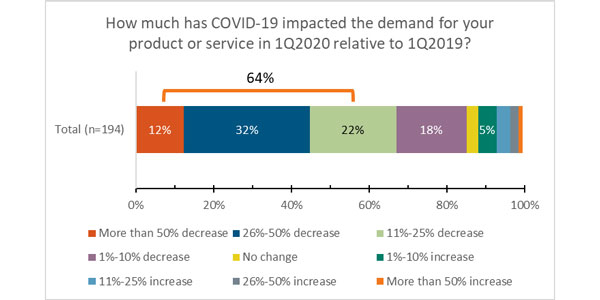

On the whole, two-thirds of aftermarket companies (64%) report demand reductions exceeding 10%, according to Fig. 2.

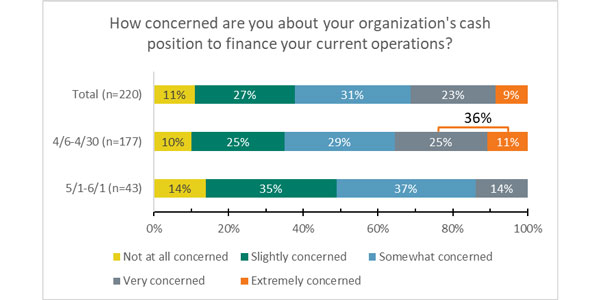

Currently, one in seven companies is highly concerned about its cash position (14% in May). This is an improvement from 36% of companies being highly concerned in April and is likely attributable to securing of government relief and adjusting to the current situation.

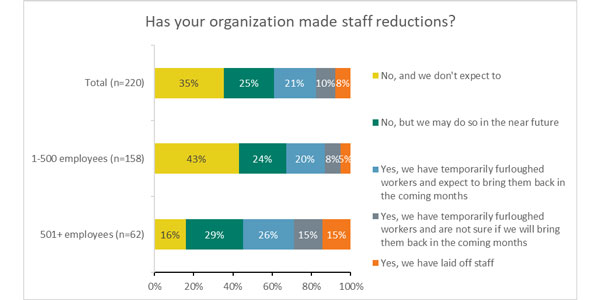

Interestingly, larger companies are more likely to have reduced staff: 56% of auto care companies with 501+ employees have laid off or temporarily furloughed workers, versus 33% of auto care organizations with one to 500 employees.

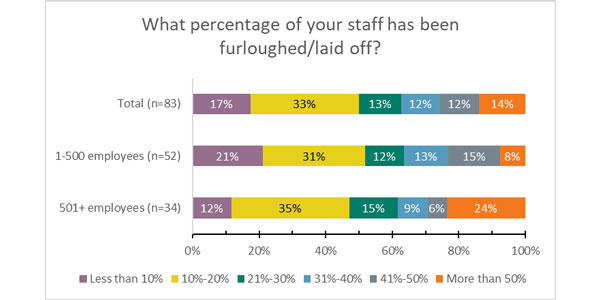

Of companies that have reduced staff count, about half have reduced staff by 20% or less, and larger companies are more likely to have reduced staff by more than 50%: Several factors are likely at play: smaller companies are more likely to be family-owned, and the decision to lay off staff may be more difficult because of close/family relations. Further, smaller companies may be required to maintain pre-pandemic employment levels to secure government assistance, and larger companies are more likely to be publicly traded, with swifter calls to action to demonstrate fiscal stewardship.

Similarly, larger companies are more likely to have closed a facility: 56% of auto care organizations with 501+ employees have temporarily closed one or more facilities, versus 16% of companies with one to 500 employees. We contend that larger companies are more likely to have multiple facilities and may need to close a facility for disinfection/deep cleaning in the event of an employee testing positive for COVID-19, and/or adjust production schedules based on shifts in product demand.

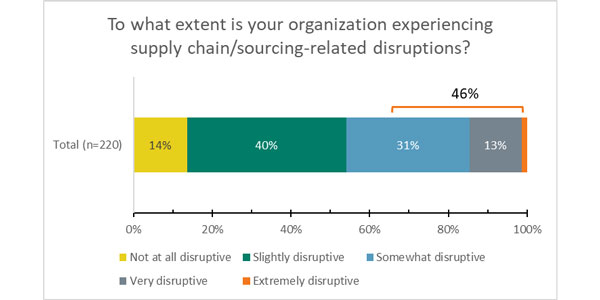

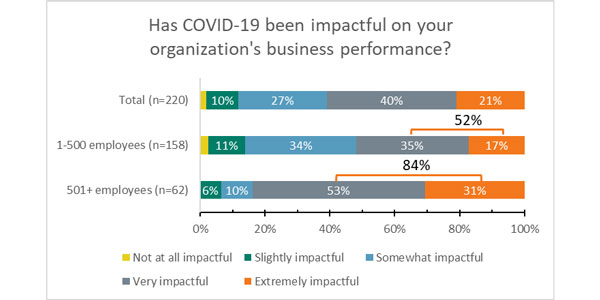

About half of the industry is experiencing supply chain disruptions (46%), and impact on business performance has been considerable, with five out of six larger companies experiencing a high level of impact (84%) compared to half of smaller companies (52%), as seen in Fig. 3.

Industry Response and Agility

With the economic upheaval fresh in our memory, shop owners and businesses have had to sharpen and modify their operations to manage cash flow, personnel and other vital aspects of their businesses in order to remain operational. Members have shared with us the challenges of staffing appropriately, particularly as business began regaining momentum in May/June. Keeping lines of communication open with your technicians is critical—being able to “staff back up,” particularly after a subsequent wave of COVID-19 cases in a state lead to tightened restrictions on activities, is essential to meet customer needs. Transparency with staff regarding anticipated reduction in hours and corresponding timelines for “ramping back up” go a long way in preserving employee loyalty.

With the possibility of increased restrictions in areas of the country with rising caseloads, auto industry managers and owners would do well to be prepared for another potential decrease in miles driven and corresponding consumer spend in the aftermarket. As many have done, positioning yourself for PPP loans, engaging your local representative (see resources at autocare.org/government-affairs/grassroots-101/) and being creative with offering innovative, customer-focused services (mobile service, vehicle pickup/dropoff, loaner vehicle, touchless service) may make the difference between businesses surviving in our “new normal” or being forced to shutter.

Mike Chung is director, market intelligence at Auto Care Association. With more than a dozen years of experience in market research, Chung and his team provide the industry with timely information on key factors and trends influencing the health of the automotive aftermarket and serving as a critical resource by helping businesses throughout the supply chain to make better business decisions. Chung has earned a Bachelor of Science in chemical engineering from Massachusetts Institute of Technology (MIT), a Master of Science in environmental health management from Harvard University and a Master of Business Administration with a concentration in marketing from Montclair State University. Mike can be reached at [email protected].